Small business group health insurance, made simple

Compare medical plans from top carriers. Get accurate quotes for your business in minutes.

Trusted by 1,000+ businesses

Get your free quote

Carriers available

How it works

Three simple steps to coverage

Enter your details

Tell us your zip code, number of employees, and contact info. Takes less than a minute.

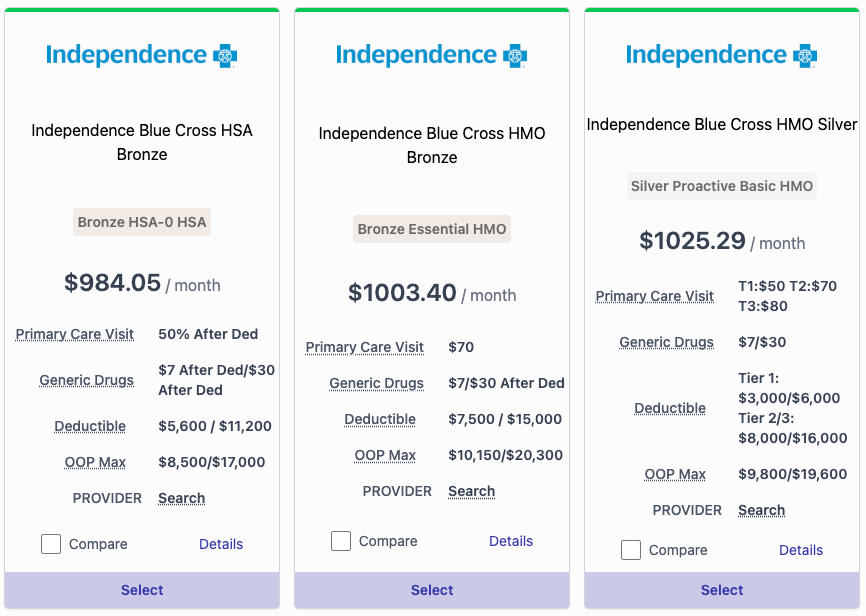

Compare plans

Browse side-by-side quotes from Independence Blue Cross, UHC, Highmark, and more.

Enroll with ease

Pick the plan that fits your budget. Our licensed brokers handle the paperwork.

Trusted by businesses across the region

Partners, affiliates, and customers across the region

Carrier partners

Why group coverage works

Built-in advantages that benefit both employers and employees

Tax Advantages

Pay Less in Taxes, Keep More Value

Use pre-tax dollars for premiums, reducing overall taxable income and lowering payroll tax burden for both employer and employees.

Carrier Shopping

Compare Multiple Insurance Providers

We shop across multiple carriers to find competitive pricing and better coverage options tailored to your group size and risk profile.

Self-Funded Plans

Maximum Savings for Healthier Groups

Pay for actual claims instead of fixed premiums. Ideal for groups with predictable usage — offering more transparency and control.

Year-Round Enrollment

No Waiting for Open Enrollment Windows

Add or update employees at any time during the year — no waiting periods. Especially useful for growing companies and seasonal hiring.

Understanding plan types

Choose the structure that fits your team's needs

HMO

Health Maintenance Organization

Lower monthly costs and deductibles with set fees for doctor visits. A primary care provider (PCP) manages your care and provides referrals to specialists.

Best for

- Lowest premiums compared to other plans

- Consistent, coordinated care

Consider

- Limited provider network

- Referral required for specialists

- Full cost for out-of-network care

EPO

Exclusive Provider Organization

Covers care from a larger network of doctors than an HMO. Premiums are higher than HMOs but lower than PPOs. Referrals may or may not be required.

Best for

- Lower premiums than PPO plans

- Large network of doctors for in-network care

Consider

- Only in-network providers covered

- Full cost for out-of-network care

POS

Point of Service

Like an HMO but more flexible — you can see out-of-network doctors at a higher cost. A PCP coordinates your care and may provide specialist referrals.

Best for

- More flexibility than HMOs

- Lower premiums than PPOs

- Flexibility to see out-of-network providers

Consider

- Higher out-of-pocket costs for out-of-network

- May still require a PCP for care coordination

PPO

Preferred Provider Organization

Maximum flexibility — visit any specialist or doctor without a referral. In-network care has lower copays and coinsurance than out-of-network.

Best for

- Broad network of providers

- See any doctor, in or out of network, without a referral

Consider

- Higher monthly premiums

- Higher costs for out-of-network care

HDHP + HSA

High-Deductible Health Plan with HSA

Lower monthly costs paired with a tax-free Health Savings Account (HSA) to pay for care. Higher deductible means more out-of-pocket before benefits kick in.

Best for

- Lower monthly premiums

- Tax-free savings for current and future health expenses

Consider

- Higher deductible before benefits apply

- Best for those comfortable with higher upfront costs

Frequently asked questions

Common questions about group health insurance eligibility and enrollment

See plans and pricing for your team — free, in 2 minutes

Free quotes, no obligation, and a licensed broker on your side.